Mark Collett

Jewish Money Saved as

Diversity Kills SVB Bank

Fri, Mar 24, 2023

[Mark Collett, leader of Britain’s premier nationalist organisation, Patriotic Alternative, discusses the story behind the collapse of Silicon Valley Bank and the usual (((goblin))) machinations within it:

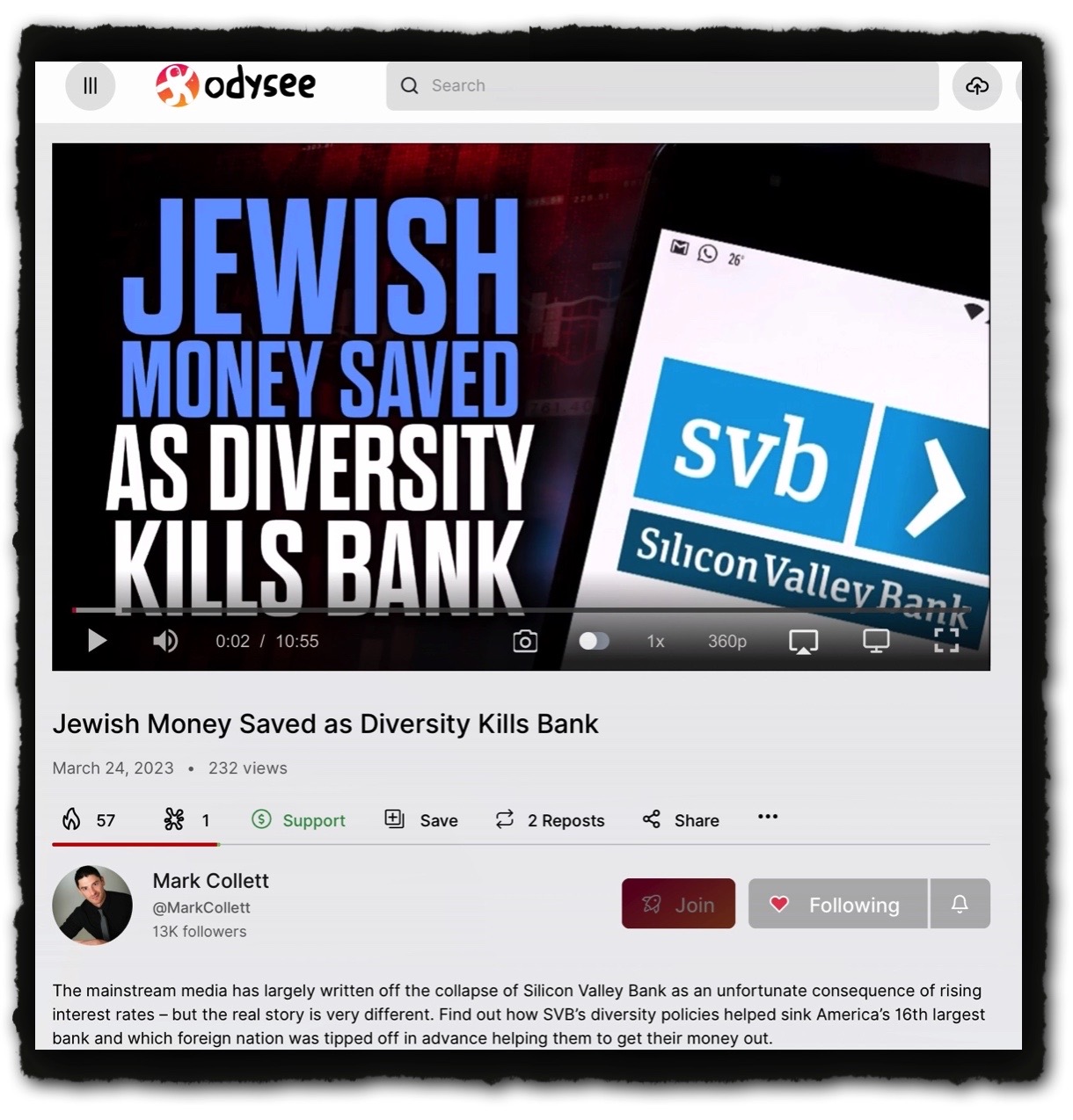

“The mainstream media has largely written off the collapse of Silicon Valley Bank as an unfortunate consequence of rising interest rates – but the real story is very different. Find out how SVB’s diversity policies helped sink America’s 16th largest bank and which foreign nation was tipped off in advance helping them to get their money out.”

– KATANA]

https://odysee.com/@MarkCollett:6/20230324—Jewish-Money-Saved-as-Diversity-Kills-Bank:4

Published on Fri, Mar 24, 2023

Description

Jewish Money Saved as Diversity Kills Bank

March 24, 2023

232 views

57

1

Support

Save

2 Reposts

Share

Mark Collett

@MarkCollett

13K followers

Join

Following

The mainstream media has largely written off the collapse of Silicon Valley Bank as an unfortunate consequence of rising interest rates – but the real story is very different. Find out how SVB’s diversity policies helped sink America’s 16th largest bank and which foreign nation was tipped off in advance helping them to get their money out.

Ways you can help contribute to my work:

BitCoin: bc1qzgjz953f4gznway0hvz6lx360yd2autdkwf6nu

Etherium: 0xb44739a8f2c57Cad38F96Aab8F2a0cA18258A7bA

BitCoin Cash: qpaaukrttfvq0j99gfl43hhs5q0tmhzfevkhp3r2c9

Monero: 42qypZQGMzNfFa5yXBxkqxL4iDw5cmzbtCC81dKcQbMrhLrsJUYAFSsLs9Um4hG32R5GfaqfgGj7oR6ZJ7pGyaY3FFu9HKD

You can also donate to my work via Entropy:

https://entropystream.live/app/markcollett

My book, The Fall of Western Man is now available. It is available as a FREE eBook and also in hardback and paperback editions.

The Official Website:

http://www.thefallofwesternman.com/

FREE eBook download:

https://drive.google.com/file/d/0B3cctZ95PDYZTnRjSUd5VUtRR2c/view

Hardback Edition:

https://www.lulu.com/shop/mark-collett/the-fall-of-western-man/hardcover/product-23388841.html

Paperback Edition:

http://amzn.eu/9LaS7HN

PLEASE NOTE: If you wish to debate with me in the comments about anything I have said, I welcome that. However please listen to the complete podcast and ensure you argue with the points I have made. Arguments that simply consist of nonsense such as “what gives you the right to judge” or “I’m a [insert religious affiliation] and you should be ashamed of yourself” or other such vacuous non-arguments will simply be ridiculed.

federal reserve; israel; silicon valley bank; svb

URL

lbry://@MarkCollett#6/20230324—Jewish-Money-Saved-as-Diversity-Kills-Bank#4

Claim ID

428caa3ef72105b2bc8cee34b9d82c0279f1774c

110.61 MB

Less

9.5K

12 comments

_____________

TRANSCRIPT QUALITY = 5 Stars

1 Star — Poor quality with many errors, contains nonsense text 2 Stars — Low quality with many errors, some nonsense text. 3 Stars — Medium quality with some errors. 4 Stars — Good quality with only a few errors. 5 Stars — High quality with few to no errors.

NOTE: Users can help improve the quality of this transcript by putting corrections in the Comment section. Thanks.

TRANSCRIPT

(10:55 mins)

And then it was gone!

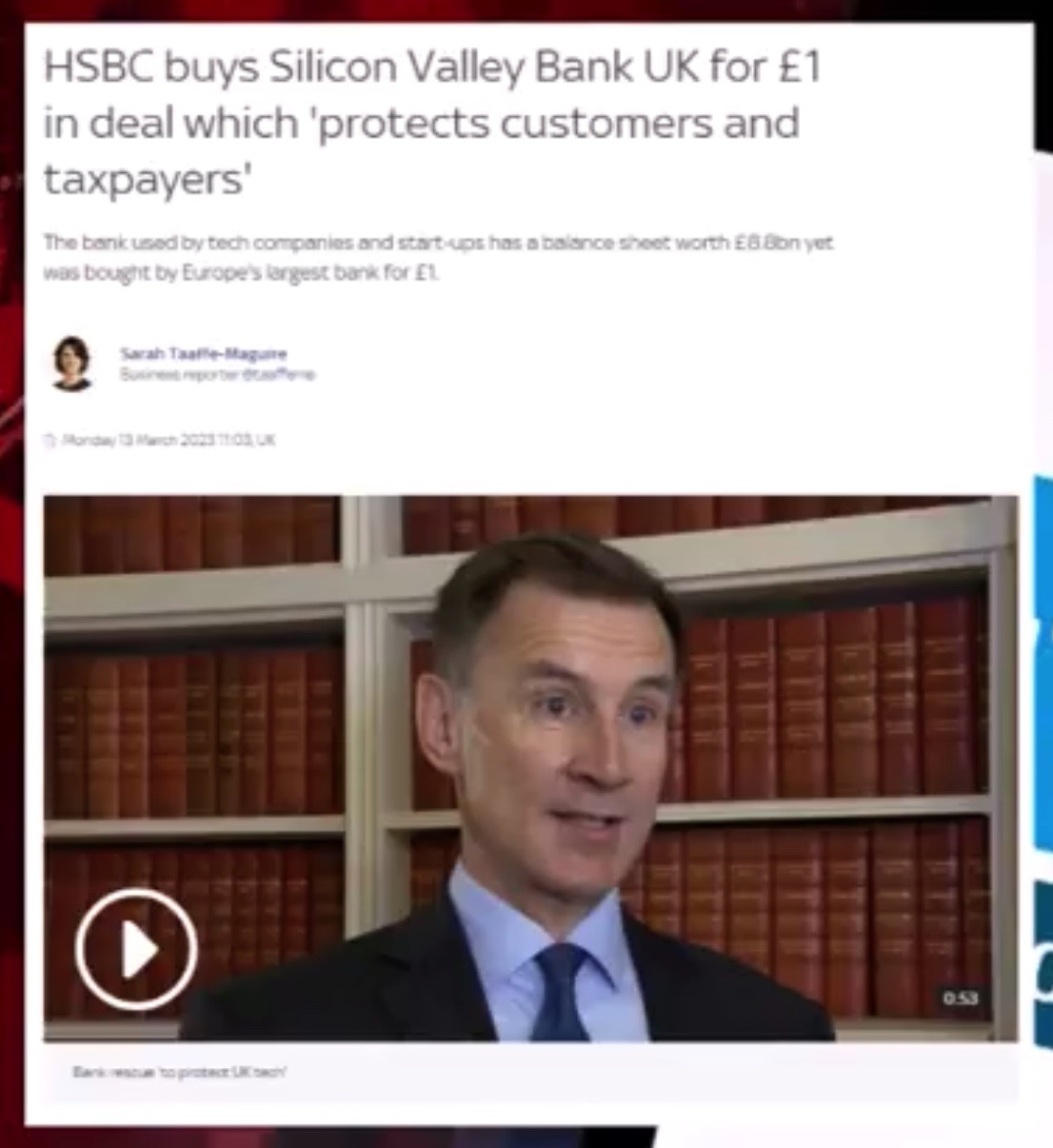

In a matter of 48 hours, Silicon Valley Bank collapsed, sending shock-waves through both the banking sector and tech industries around the world.

SVB assets were frozen as US regulators swooped in and took control of the California-based bank after customers began withdrawing their money en masse amid fears over the bank’s financial health!

This run on the bank left SVB branches closed as customers waited anxiously to find out whether their money would be safe or whether they had lost everything!

But how did SVB get to this point? What could have led to such a collapse and what does this mean for the health of the American economy?

Well, the easy answer to this is rising interest rates. The Federal Reserve has been repeatedly forced to raise interest rates to stem rising inflation caused by the long-term US Government policy of printing trillions of dollars and handing out free money in order service the ever-growing welfare time-bomb that sits ticking ominously under the American economy.

So, does that give SVB a pass in all this? Was Silicon Valley Bank just collateral damage thanks to widespread macro-economic mismanagement?

Oh no!

Silicon Valley Bank wasn’t killed by rising interest rates. SVB was killed by a mixture of poor investment practices coupled with their own diversity policies which left the bank with major structural failings which were brutally exposed the moment economic conditions were no longer favourable!

Al Jazeera ran an interesting article on SVB’s collapse which sheds a little light on how SVB structured their investments and why their investment policy placed them at risk.

I read from that article, and I quote:

“SVB collapsed because of a stupid rookie mistake with their interest-rate-risk management. They invested short-term deposits into long-term bonds. When interest rates rose, the value of the bonds fell, wiping out the equity of the bank – James Angel, an expert on regulation of global financial markets at Georgetown University, told Al Jazeera.”

End quote. SVB had ploughed billions into US government bonds during the era of near-zero interest rates.

And that policy, which had seemed like a safe bet, quickly became a gargantuan blunder as the Federal Reserve raised interest rates aggressively in an attempt to get inflation under control.

But when interest rates rise, Bond prices fall, so the jump in rates eroded the value of SVB’s Bond portfolio. Once SVB’s position became known, panic spread like wild fire and there was a good old-fashioned run on the bank and customers began withdrawing their money as quickly as they could.

However, thanks to SVB’s reliance on long term bonds – bonds that can only be liquidated quickly at a huge loss, SVB didn’t have the available funds to cover the withdrawals and their only way to realise such funds would have been to take even larger loses, and within two days, it was all over.

But who were these “geniuses” that had placed all their eggs in one basket and doubled down on these long-term investments? And whilst we are at it, what other policies did theses “geniuses” endorse?

Well, it wasn’t just SVB’s policies on long term investment’s that led to the bank’s collapse. It was the bank’s entire internal structure that was at fault. In short, SVB executives seemed to place a greater emphasis on pushing diversity and liberal values than they did on securing the deposits of their customers and realising returns on investment.

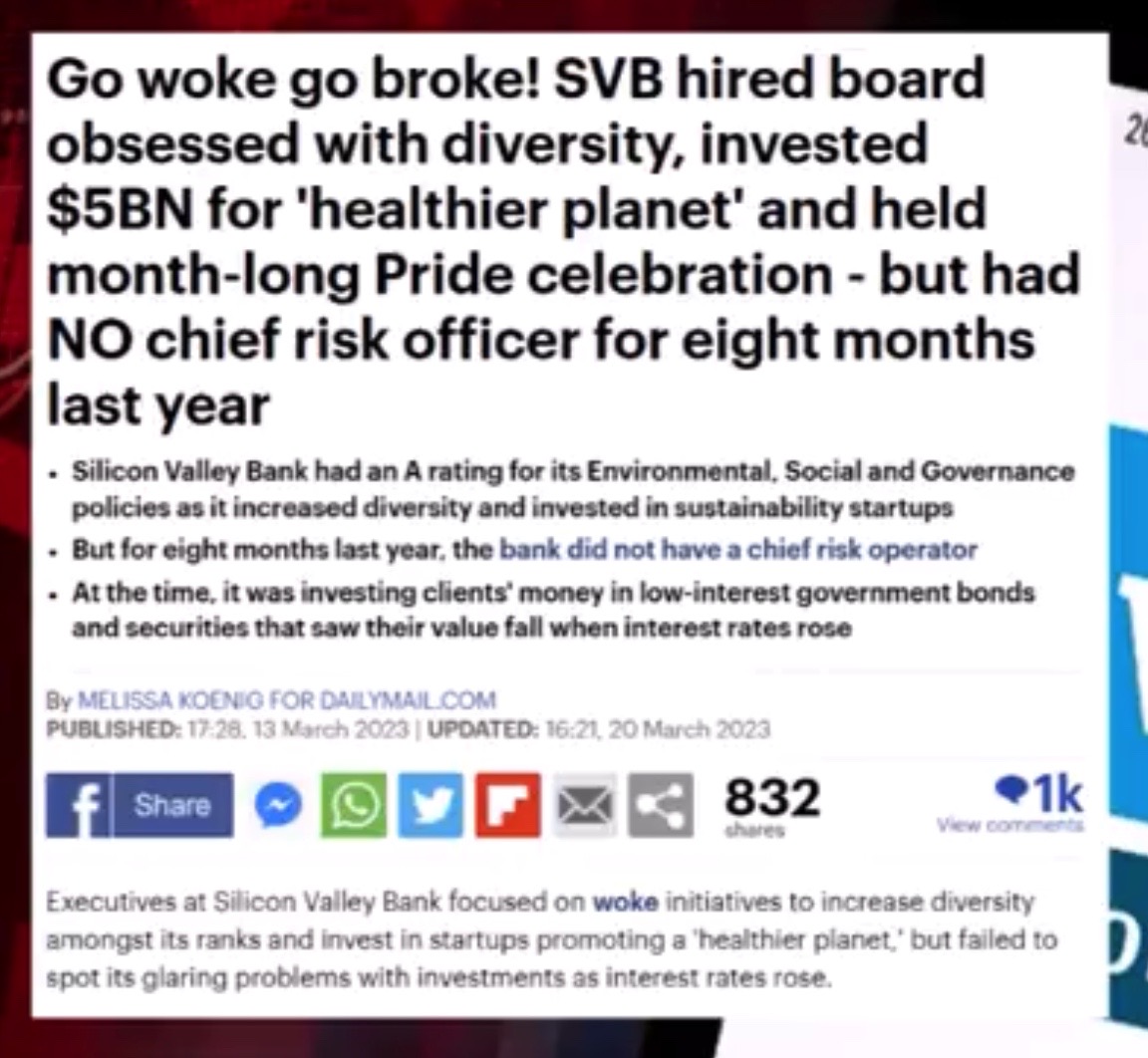

I read this from the Daily Mail, and I quote:

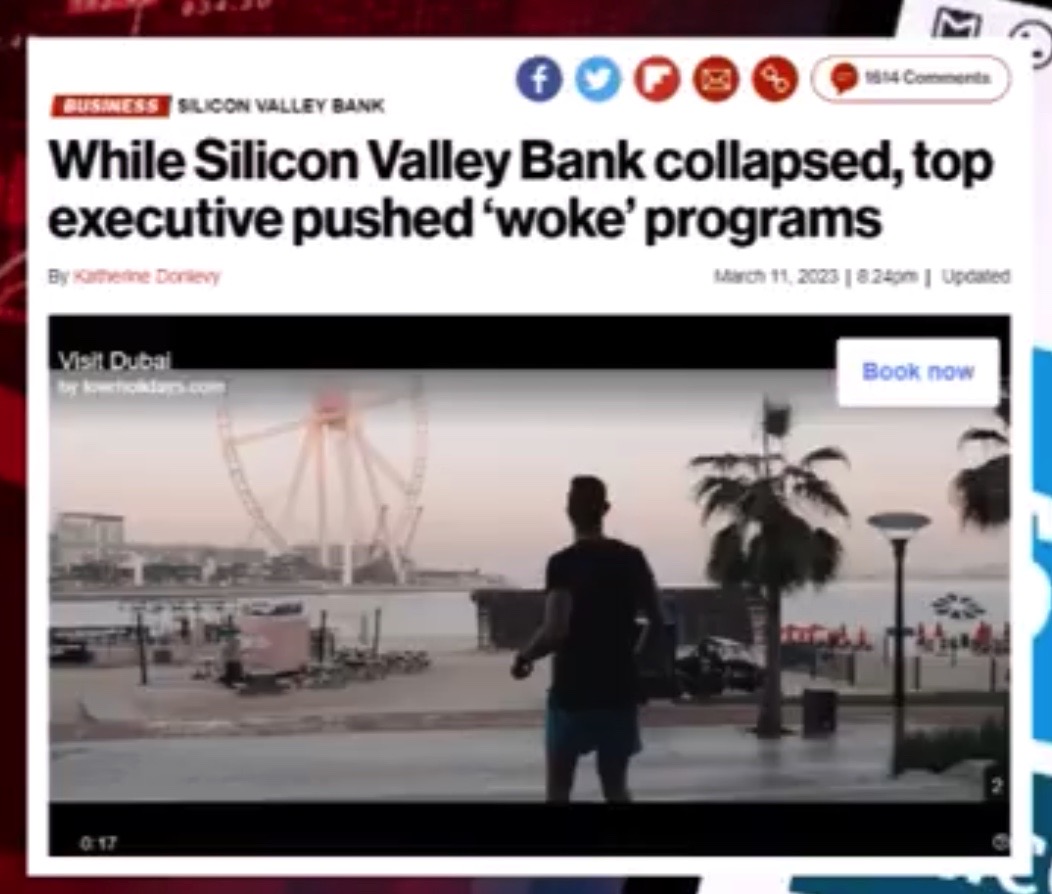

“Executives at Silicon Valley Bank focused on woke initiatives to increase diversity amongst its ranks and invest in start-ups promoting a ‘healthier planet’, but failed to spot it’s glaring problems with investments as interest rates rose.

The now-failed bank had an A rating for it’s Environmental, Social and Governance policies according to the MSCI index after creating it’s own initiatives to ‘advance inclusion and opportunity in the innovation economy’ and investing in clean energy solutions over the past few years.

It even announced that it would invest a whopping $5 billion by 2027 to support sustainability efforts, while it’s European offices held a month-long Pride celebration and promoted ‘safe spaces.’

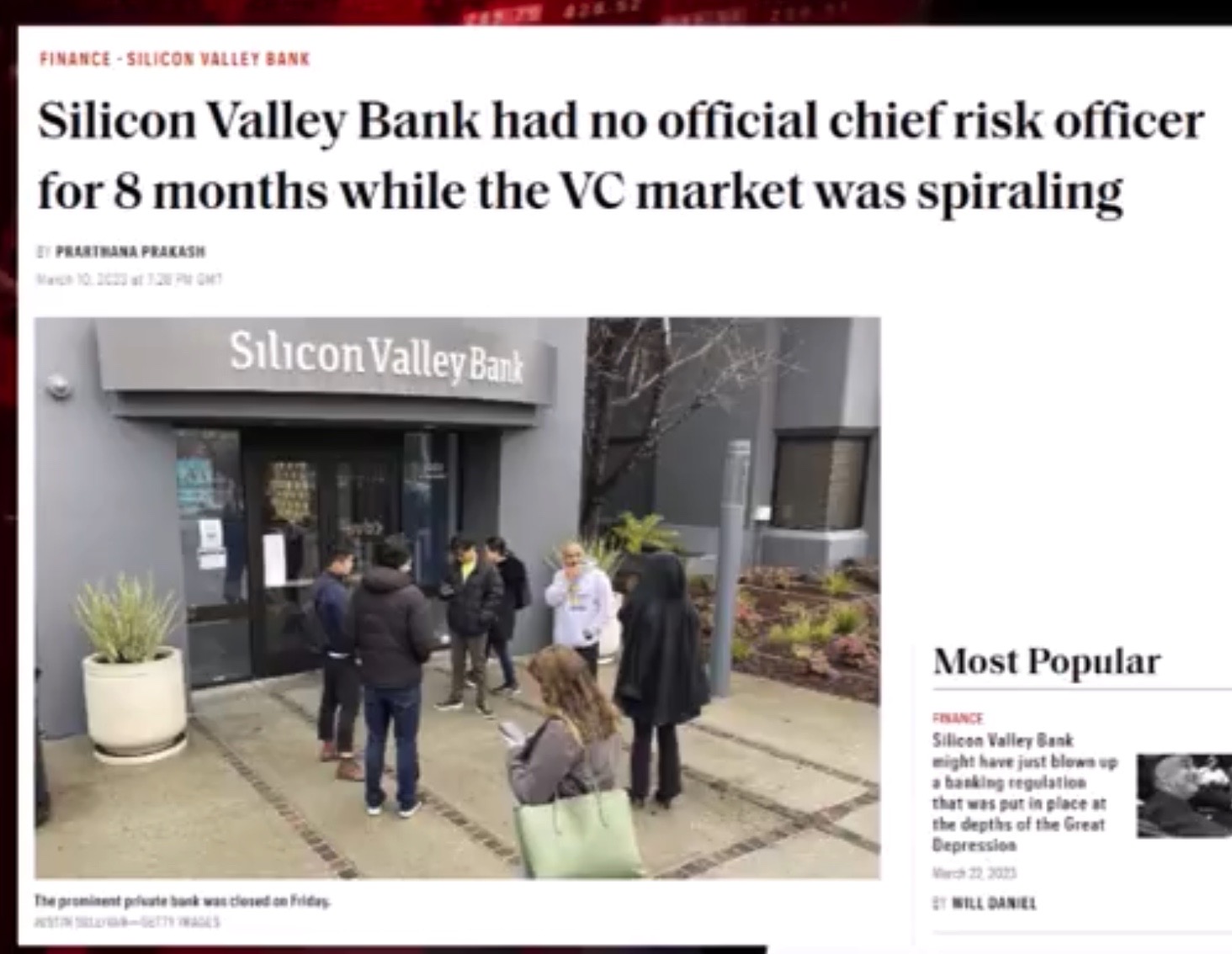

But for eight months last year, the bank did not have a Chief Risk operator, as it invested clients’ money in low-interest government bonds and securities.”

End quote. In a very real sense, Silicon Valley Bank committed suicide via self-immolation.

Everything that the bank’s executives did was geared around virtue signalling and promoting progressive causes. But rather than covering themselves in glory, they metaphorically covered themselves in petrol and unfortunately for them, rising interest rates were the lighted match that ended up setting SVB ablaze.

But who were these aforementioned “geniuses” that were making poor investment decisions whilst focusing on “diversity” and “inclusion”. Well, curiously the bank seemed fond of employing people based on their progressive agenda, rather than on the basis of merit – so to put it politely, the team of “geniuses” running SVB weren’t exactly the best people for the job!

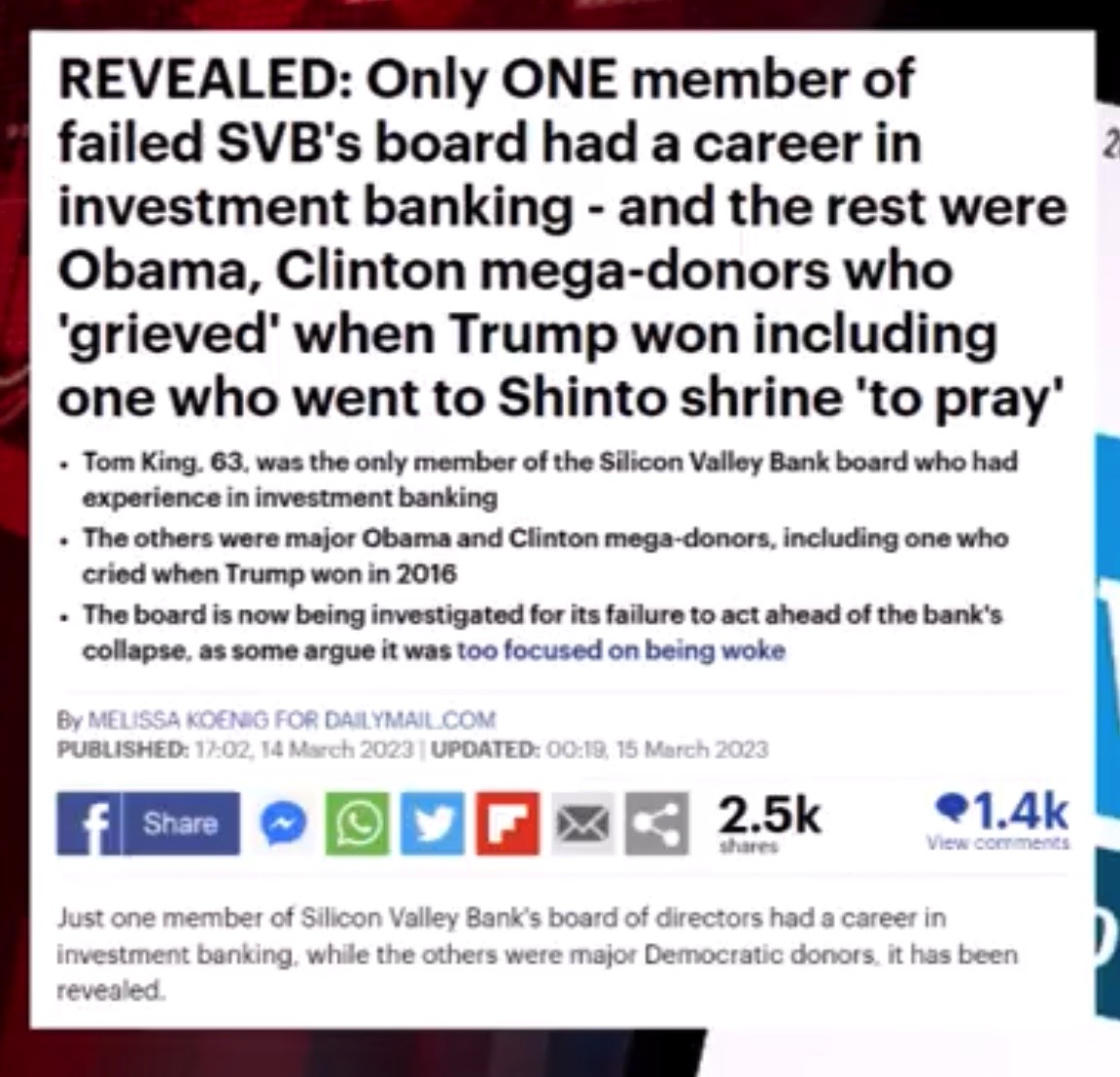

The Daily Mail reported the following, and I quote:

“Only one member of failed SVB’s board had a career in investment banking – and the rest were Obama, Clinton mega-donors who ‘grieved’ when Trump won including one who went to Shinto shrine ‘to pray’”.

End quote.

So not only did the company lack a chief risk assessment officer, but those at the very top of the organisation had no real history in the financial sector and seemingly didn’t have a clue what they were doing – which seems a little crazy considering they were playing with billions of dollars of their customers money. But hey, who cares about billions of dollars of deposits when there’s virtue signalling to be done?

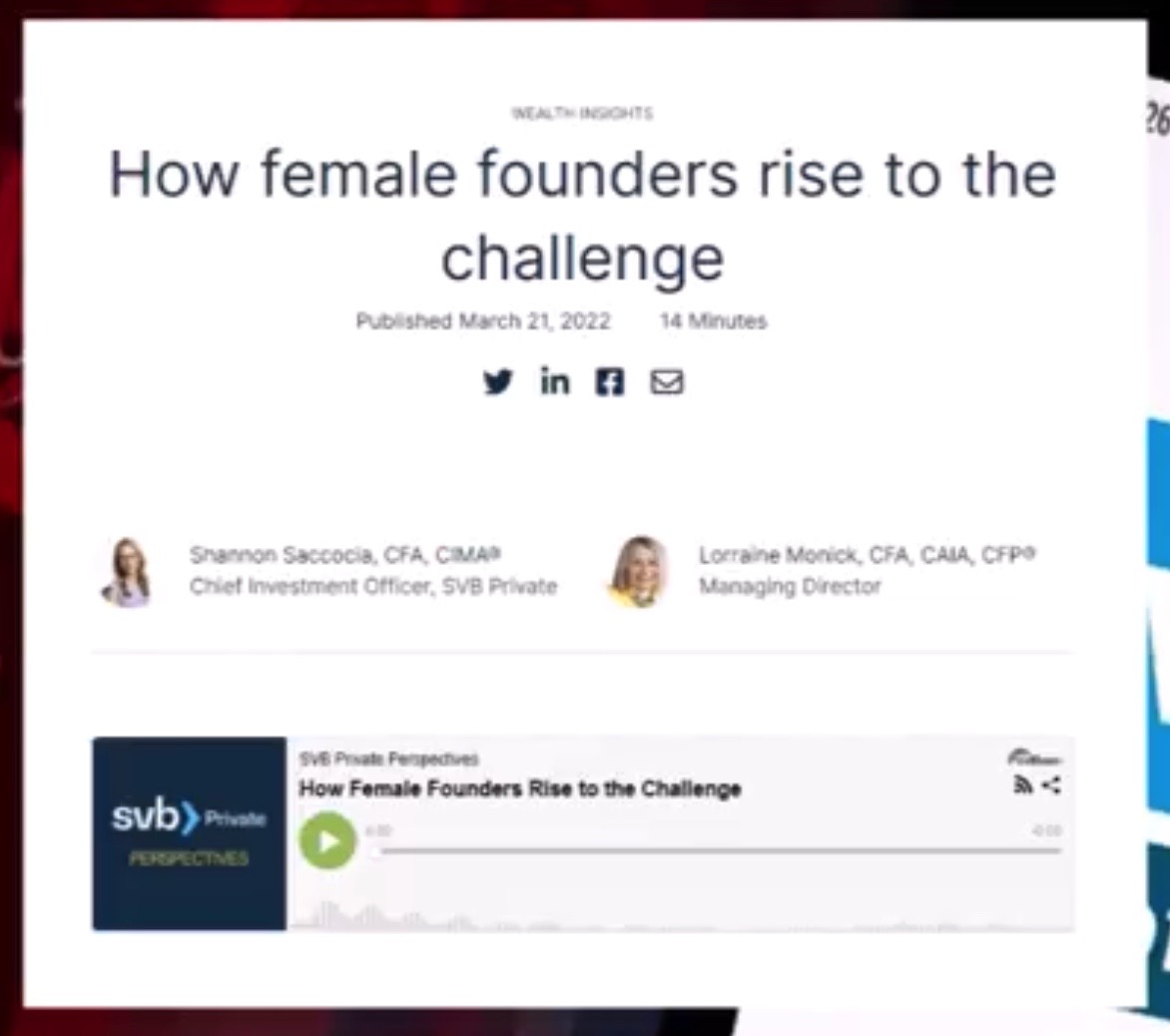

So, what did these board members spend their time doing? Well last year, the company’s Chief Investment Officer, Shannon Saccocia, and it’s Managing Director, Lorraine Monick, managed to take time out their hectic schedule to record a self-serving podcast about how “female founders rise to the challenge”, at the time of publication this wonderful little snippet of progressive thinking is still available on the SVB website!

Superb stuff! A lecture from the chief investment officer on how she was rising to the challenge. But the only challenge she appeared to succeed in was destroying America’s 16th-largest bank.

But let’s put this collapse into perspective by talking numbers. How much money was the 16th largest bank in the US managing? Well, as of December 2022, SVB had $209 billion in assets, and $175.4 billion in total deposits, according to the Federal Deposit Insurance Corporation. This is not an inconsiderable sum of money. But compared a larger banks like JP Morgan Chase which manages $3.67 trillion worth of assets, SVB’s worth is a mere drop in the ocean.

So, it’s clear to see that diversity hires and virtue signalling does not a stable nor profitable company make! And that SVB’s progressive policies sealed the bank’s fate!

But what about the wider implications of this collapse? Do I think SVB’s demise will lead to a wider banking collapse and a financial implosion? No, I don’t.

I think SVB will simply be gobbled up by the larger banks, it’s losses written off by the US Government, it’s clients bailed out and business will continue largely as normal with one small change – the banking sector will have one fewer operator, and as such, power will be concentrated in the hands of even fewer people.

Which is always what happens in these cases, a banks closes, it’s gobbled up and power always becomes more centralised and is placed in the hands of a smaller number of people who now collectively wield slightly more power and influence.

Is this good for normal people? No it isn’t. It leads to less choice; it leads to a further centralisation of all banking services and it is likely just another small step down the road toward a central digital currency.

But don’t despair, it’s not all bad news!

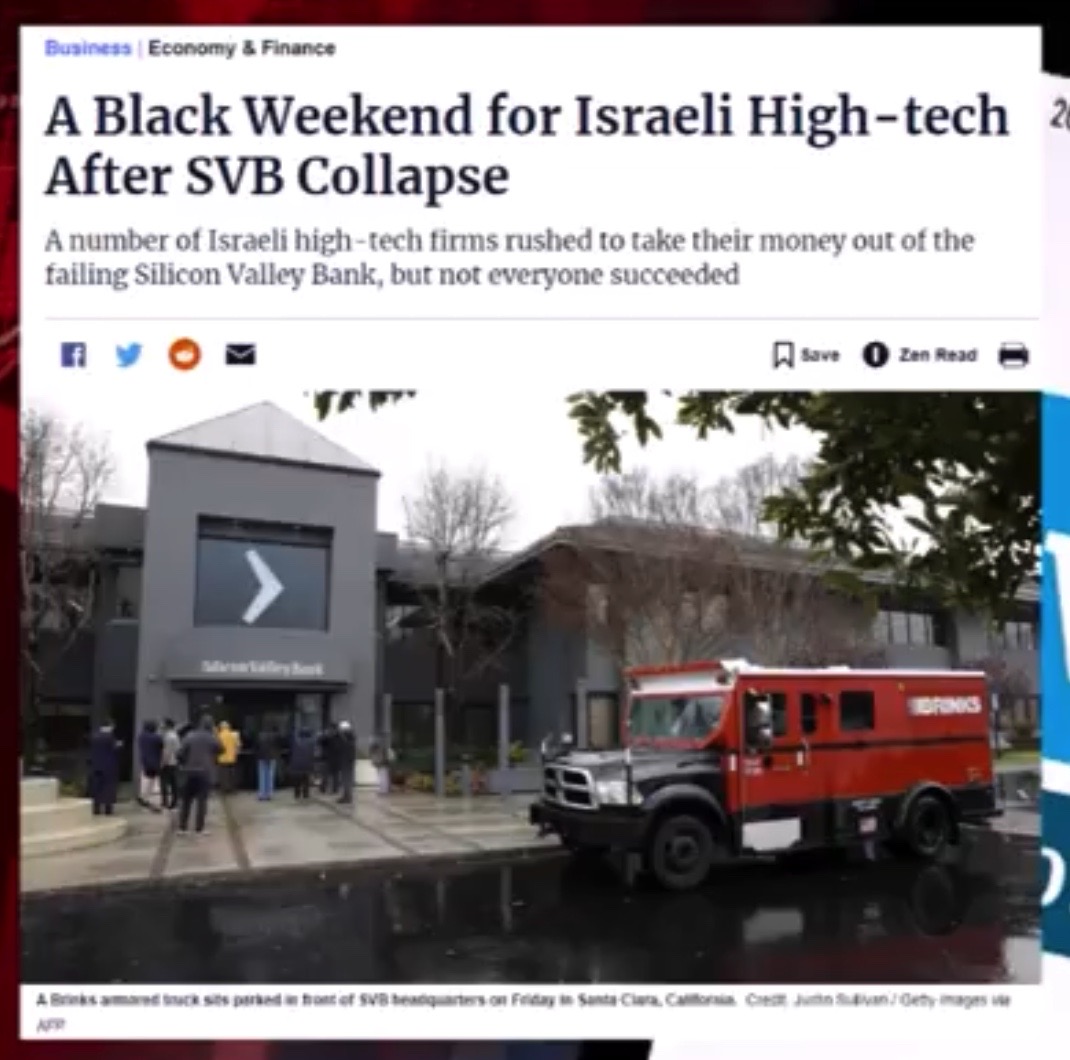

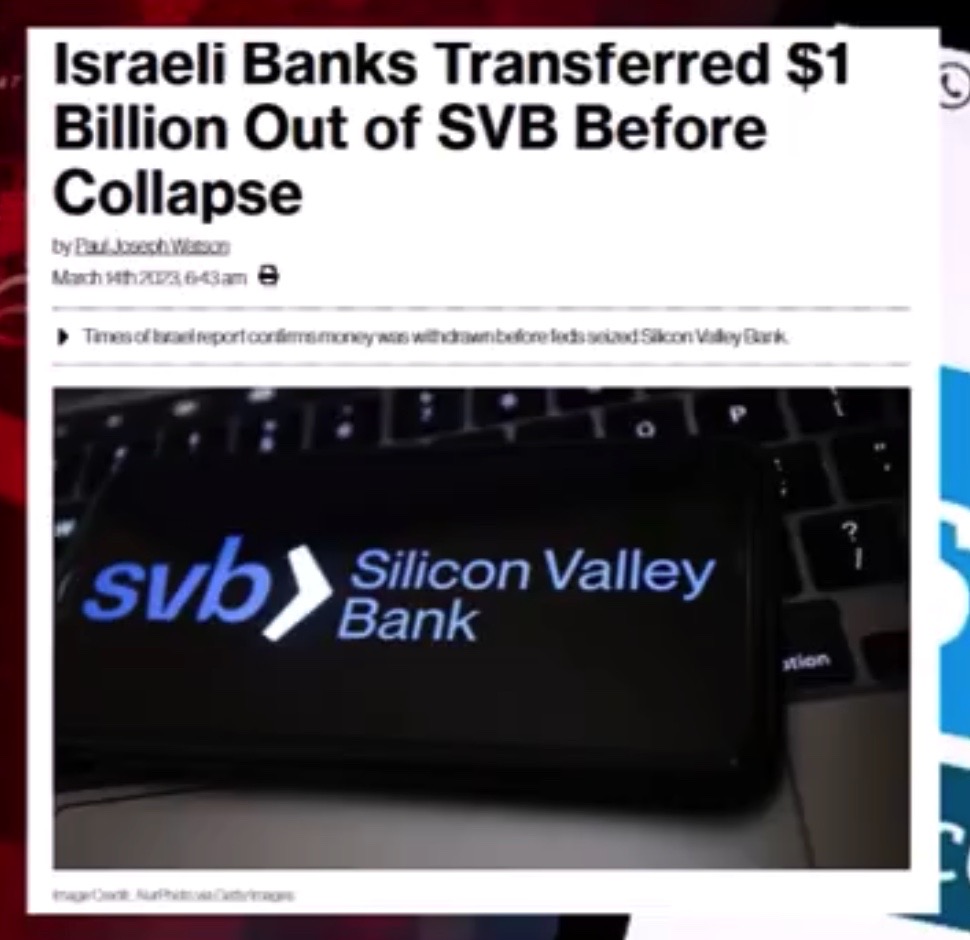

Israeli companies were tipped off about SVB’s impending doom and managed to get their money out of the bank before it collapsed! I bet that makes you feel better about this situation! Haaretz had the following to say, and I quote:

“Several Israeli companies rushed to get their money out of SVB and move it to other banks in the United States and Israel. According to LeumiTech, it’s teams helped it’s customers move about $1 billion to Israel.

People in the industry said at the end of the week that a good many Israeli companies had been able to get their money out in time, but that it was clearly not the case for everyone.”

End quote.

How reassuring to know that leading SVB and industry insiders used their knowledge to ensure that it was Israeli companies that managed to get their money out safely before the shutters came down!

It’s almost like there’s a group of people who play a disproportionate role in the banking and financial sector and who like to gamble with our money but when things go wrong, they always look after their own first; leaving everyone else to deal with the unfortunate fallout.

But be careful, saying that might result in you being branded a conspiracy theorist!

[10:55]

END

============================================

Odysee Comments

Redpill Rundown

1 hour ago

Go woke, go broke?

4

0

Hide replies

robomartion

1 hour ago

go woke go broke!

2

0

@piggu

1 hour ago

Goy broke.

2

0

Htrac

1 hour ago

Woke self-destruction is the norm now. The West as a whole is committing suicide.

1

0

@DeezKosherNuts

1 hour ago

Mark is good at making short videos that sum things up.

1

0

@BritishGammon

32 minutes ago

10:27

Well, I guess that makes me a conspiracy theorist then. 😂

1

0

Dirty Thirty

1 hour ago

o/

1

0

Peak Aussieman

1 hour ago

Oy Vey My Goy! Mi Shekels need a savin.

1

0

robomartion

1 hour ago

I wouldn’t be surprised if it was all carefully planned and curated

1

0

@Spectromancer

18 minutes ago

I don’t think those women were hired to do real work. The entire “collapse” was really a robbery.

@Gundobar

1 hour ago

the more you know

@Grumpole

1 hour ago

Invest in bullshit only gets you more excrement.

0

0

==========================

See Also

Mark Collett — It’s Okay To Be White — TRANSCRIPT

Mark Collett — Christmas Adverts – Multicultural Propaganda — TRANSCRIPT

Mark Collett — What We Must Do To Win — TRANSCRIPT

Mark Collett — Assad Didn’t Do It – Faked Syrian Gas Attack — TRANSCRIPT

Mark Collett — The Plot to Flood Europe with 200 Million Africans — TRANSCRIPT

Mark Collett — The jewish Question Explained in Four Minutes — TRANSCRIPT

============================================

PDF Download

- Total words in post = 2,187

- Total words in transcript = 1,568

- Total images = xx

- Total A4 pages = xxx

Click to download a PDF of this post (x.x MB): (Available later)

Version History

Version 5:

Version 4:

Version 3:

Version 2: Sat, Mar 25, 2023 — Added images.

Version 1: Sat, Mar 25, 2023 — Published post. Includes Odysee comments (12).