Monetary Institute

Today’s Source

of Money Creation

Mon, Feb 5, 2018

[Professor Richard Werner gives an overview of how money is created (via Credit Creation) in nations throughout the world and the impacts and consequences of the current system, and how we need to move towards smaller localised banks that create credit for productive purposes, not financial speculation and manipulation.

Central banks meanwhile seek more and more power in ways that will lead to an Orwellian level of control over the individual.

– KATANA]

https://www.youtube.com/watch?v=IzE038REw2k

Published on Mon, Feb 5, 2018

Description

0:14 / 15:34

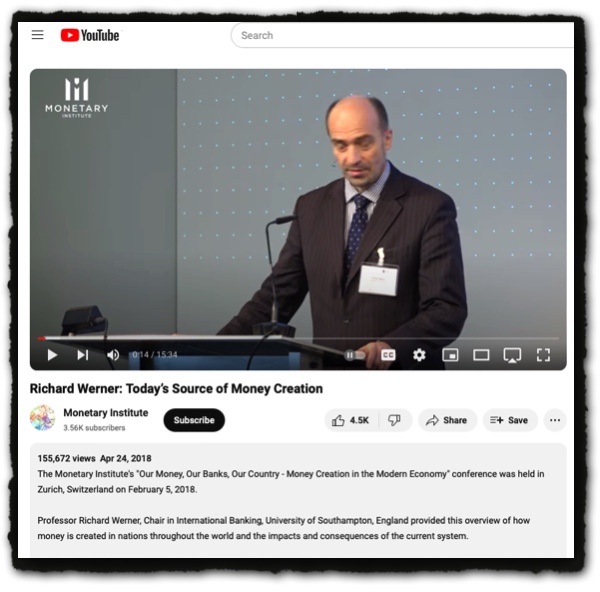

Richard Werner: Today’s Source of Money Creation

Monetary Institute

3.56K subscribers

Subscribe

4.5K

Share

Save

155,672 views

Apr 24, 2018

The Monetary Institute’s “Our Money, Our Banks, Our Country – Money Creation in the Modern Economy” conference was held in Zurich, Switzerland on February 5, 2018.

Professor Richard Werner, Chair in International Banking, University of Southampton, England provided this overview of how money is created in nations throughout the world and the impacts and consequences of the current system.

Transcript

Follow along using the transcript.

Show transcript

Monetary Institute

3.56K subscribers

Videos

About

5 Comments

_____________

TRANSCRIPT QUALITY = 5 Stars

1 Star — Poor quality with many errors, contains nonsense text 2 Stars — Low quality with many errors, some nonsense text. 3 Stars — Medium quality with some errors. 4 Stars — Good quality with only a few errors. 5 Stars — High quality with few to no errors.

NOTE: Users can help improve the quality of this transcript by putting corrections in the Comment section. Thanks.

TRANSCRIPT

(Words: 2614 – 15:34 mins)

It’s a pleasure to be here. Thank you for the invitation. And I would like to go straight into my presentation about the source of money creation and it’s allocation. And the underlying issue is, “central planning versus decentralised decision making”.

Now, banking actually has not been very well understood. There have been three theories of banking. And they’ve existed and coexisted for at least the past century.

The most dominant one currently is still the Financial Intermediation theory of banking.

And nobody had ever done an empirical test. So I thought:

“Well, you know, since these theories are mutually contradicting when it comes to the crucial question of where does the money come from when you get a loan from the bank?”

Well, let’s figure it out. Let’s do an empirical test. So I did this and published 2014 and, 2016, two papers.

The conclusion is the Financial Intermediation theory was rejected. Banks are not financial intermediaries.

You may have heard of the Fractional Reserve theory, slightly older. That one was also rejected. It says that banks lend money out of reserves. And they don’t!

Financial Intermediation theory says they lend out of other people’s deposits. And they don’t!

So the oldest theory was the one that was found to be correct. And that’s the Credit Creation theory, which was known 100 years ago, which is why one of the papers is called lost century. In economics, banks create money out of nothing through the process of credit creation.

I know there’s some lawyers and experienced lawyers in the room, and actually, the law helps a lot to understand banking, because at law, it’s very clear. Banks are essentially the opposite of what economists have claimed. Economists always say banks are:

“Deposit taking institutions that lend money.”

Banks don’t take deposits and they don’t lend money. They don’t take deposits because they borrow from the public. A deposit suggests something held in custody, a bailment. And this is not what happens.

Instead, the money that you lend to the bank, which they call erroneously a “deposit”, is actually their money. They own it. It’s just a loan. You’re a general creditor.

And banks never lend money because, and that’s unlike firms and non-bank financial institutions. They are in the business of purchasing securities. When you get a loan, the loan contract is a “promissory note”, just like the Bank of England promissory note. Of course, not legal tender, as you may have noticed.

But the bank will purchase that security from you. That’s what it does. And now it owes you money, and it creates a record of the money it owes, which we call “deposits”.

And that’s how the money supply comes about.

[03:04]

So you get a loan, 1,000 pounds, let’s say. And the loan contract is purchased by the bank. It increases the bank’s assets, and the bank then records the money it owes you, which it calls slightly incorrectly, a “customer deposit”. Because no customer has deposited this, and in fact nobody has deposited this anywhere. It’s not transferred from anywhere inside or outside the bank. It’s created out of nothing. These fictitious deposits are our money supply.

So banks are special. They create the money supply, 97% in most countries of the money supply out of nothing, through the process of what’s called “credit creation”.

That’s of course also why actually central banks have been all along monitoring bank credit quite carefully, whether they announce this or not. And they’ve been guiding bank credit.

And of course central bankers have been quite aware of these facts.

Now the recognition of bank credit creation is a game changer to solve many of the world’s problems, such as the recurring banking crises can be prevented. Unemployment can be solved. Business cycles, underdevelopment, depletion of finite resources, all these problems can be solved by utilising the power of bank credit creation.

And this is something we think about before we decide to abolish it. Because this power can be harnessed.

So can we achieve high sustainable, stable growth and development without crisis? Yes! This is the fundamental basics. This is how the economy really works.

So the money supply is actually Credit, let’s call it “C”. And we have to disaggregate it because the crucial thing is who gets the money for what purpose. Simple dis-aggregation into the real economy, CR and the financial transactions, financial economy, CF.

So if banks create credit used for financial transactions, the left side. This is of course one example of unproductive credit creation. You’re pushing up asset prices. This explains in aggregate asset bubbles and all the large asset movements. It’s simply credit creation for asset transactions. That’s not part of GDP, because GDP is value added. And of course that doesn’t add value as a zero sum game.

But it will create banking crises. Because once you’ve pushed up asset prices by 300, 400%, they just need to drop by 10%, and the banking system is bust because equity is less than 10%..

Now when banks create credit for the real economy, for real transactions, we still have two scenarios. One is easily understood. If they create credit for consumption, you suddenly have more demand for consumer goods. And if they do a lot of that, of course you get consumer price inflation. That’s what most people think of as the central scenario. Well, it’s actually only one of three. And the one that we understand best and really not the most burning one, because it’s been financial credit.

But there’s a third scenario and that’s when banks create credit for the real economy, but it’s used for business investment in the creation of new goods and services, productive investment or implementation of new technologies that creates growth without inflation and without crises.

[06:20]

And as long as you ensure that bank credit creation is used for the green box, you get high growth, no crises and no problems.

So why haven’t the central planners at the central banks ensured that? Well they have in some countries, but not in others.

And I think that’s really the first issue we have to address. There’s more to this and of course in twelve minutes I won’t have time to address this.

But if you split this credit creation, you can explain GDP growth very nicely in many countries. Asset prices. Japanese asset bubble is just credit creation for asset transactions. When this doubled from 15% to 30% of total credit, that was the 1980s bubble and Japan is still trying to get over that.

So total bank credit in Japan was expanding at massive growth rates, way ahead of nominal GDP. Going into asset markets. You didn’t have to be a rocket scientist to know that a banking crisis was coming next.

So the wrong allocation of money creation for asset purchases, that is the problem. And we need instead productive loans for business investment.

So the key question is who should make this decision? It seems the regulators, the central banks, actually had forgotten to tell the banks:

“Oh by the way, you should only create a productive credit for sustainable business investment.”

That way we could have prevented all these boom-bust cycles and crises and all the inequality that’s been created as a result of this.

So now that we’ve uncovered this, what should we do? Who should make this decision? So the question is not really “banks versus central banks”. Should we take the privilege to create money from the banks and give it to the central banks? It’s really “centralisation versus decentralisation”.

Should this decision be made by central planners or in a decentralised market based fashion? What’s the scientific way to tackle this?

Well, let’s look at the empirical evidence, let’s look at the historical record.

So what’s the evidence on centralised decision making? The idea to abolish bank credit creation and centralise the decision of the quantity and allocation of the money supply in the hands of one group of central planners is not a new one! That’s how the Soviet Union ran it’s economy for half a century. That failed spectacularly!

So let’s keep that in mind. China, by the way, learnt the lesson. Deng Xiaoping from 82 onwards, changed it’s financial system and introduced banks, introduced decentralisation with hundreds, if not thousands, of banks creating credit locally and making that decision locally.

And of course China thrived and the economic miracle of double digit growth was based on that. In fact, it used window guidance of bank credit to suppress in a high growth phase the financial credit and the speculative and the consumption credit.

[09:08]

Another example, evidence of centralised decision making, the UK. Now the UK has a very centralised and concentrated financial system because just five banks, who as we know, collude in many ways and fix things, make all the decisions. 90% of deposits are with them. So centralised decision making in the London headquarters has not delivered very good results.

By the way, there’s reports on this has been recognised again a century ago:

“The big five dominating, lack of competition, the big five failed to provide long term investment.”

All these things were announced in a report in 1918! Of course, could have been written yesterday.

So if you look at bank credit in the US, sorry, in the UK, then 90% is “Asset Credit creation”. So credit for financial circulation is CF. And of course that’s no good!

And that’s the problem of centralised decision making. The central planners like an easy life and they think that’s good for them. It’s not good for the economy.

Another piece of evidence on centralised decision making is the ECB in the 2000s. So credit creation in Spain, Ireland, Portugal and Greece was expanding by 30, 40% under the watch and auspices and supervision of the ECB. As I had warned the ECB was going to do this, create asset bubbles, banking crises and recessions in the Eurozone.

And of course that’s what it did!

So again, the problem of centralisation in the hands of these central planners.

Another example, Japan in the eighties, they used the window guidance, credit guidance tool until the eighties for good purposes.

But then the central planners, because they’re unaccountable and too independent, decided:

“Oh, let’s create a bubble!”

And they announced their window guidance loan growth targets. And then pressed the button, you see the actual results three months later. Banks had to follow and they had to increase their lending for real estate speculation.

And that’s how the Japanese bubble was created by the Bank of Japan.

So centralised decision making has failed. The evidence of decentralised decision making is from China, as I mentioned briefly. And Germany. Germany actually has been very successful in its economy for 200 years. And its exports are often larger than Chinese exports, although the population, only 6% of the Chinese population. How is that possible?

In fact, if you look at market champions, these are companies that are number one, two or three in terms of market share globally. And hidden champions are small firms that are global market leaders. Global champions! Germany has the largest number of hidden champions, small firms that are global market leaders by far of any country. The US comes second, Japan and so on.

How is that possible? Most exports from Germany are from small firms, family owned businesses. Well, it’s because of the community banks and the community banks. In Germany there’s 1500, the largest number of banks in the European Union. Big banks lend to big companies, small banks lend to small firms. Germany has lots of small banks. Decentralised decision making. That’s been highly successful. 70% of banking, the green two segments are with not for profit community banks. We already have public money creation, in the form of local community banks, not for profit banks. So that’s unique in the world. And that’s delivered high growth without the bubbles.

[12:48]

So central bankers create cycles. How have the central bankers – this is my last slide because my twelve minutes is just up – have reacted to the truth coming out? They admit that they’ve been telling porkies [lies]! And now they propose to increase their power. So central bankers belatedly admit:

“Oh, now that you’ve mentioned it, yes, banks create the money supply, so let’s abolish that now!”

“And also, by the way, let’s abolish cash! So what should we do? We’ll introduce digital cyber currency that central banks issue and control and thereby gain total control over all economic transactions, decisions and the whole lot!”

You’ve just heard from the CEO of the GDI.

So the greatest concentration of central banking power in history is really the bid they’re aiming at. That’s the central bank’s goal!

And of course, digital accounts of dissenters and regime critics could be switched off! It would be very difficult to even purchase necessities.

So this is an Orwellian dystopia of total control, the end of any freedoms! That’s really what central banks are aiming at.

Several central banks have, like the Bank of England, already prepared their microchip implant, RFID chip, to be implanted under your skin. And why is the sudden discussion about Universal Basic Income from all the grassroots and inverted commas “movements” and billionaires? Oh, Universal Basic Income is the bribe for you to accept the microchip.

The overarching trend of the 20th century is concentration of power in the hands of the few. That’s what we have to keep in mind. We have to work against this. We don’t want to have these unaccountable central planners making decisions.

We need decentralisation, and the solution, therefore, is to maintain public money in the hands of local community banks. Decentralised decision making give local people the power in the form of local public banks and local not for profit community banks.

As I walked in, I was delighted to see that the Gottlieb Dutwaller Institute is also about genossenschaften cooperatives.

And of course, the majority of banks in Germany are cooperative banks. That’s really what we need.

So we shouldn’t really abolish banks. We just have to get rid of the “too big to fail banks”, introduce a few rules that you create credit for productive purposes, and then we can solve many of the world’s problems.

And these are really the promises of economics, that we can solve a lot of mankind’s problems. As JFK said:

“Our problems are man-made, therefore, they may be solved by man, and man can be as big as he wants!”

Of course, he was referring to ladies as well, no doubt:

“No problem with human destiny is beyond human beings – JFK.”

Thanks very much.

[applause]

[15:32]

END

============================================

Youtube Comments

(Comments as of 5/3/2024 = 5)

@valdopetronio4262

5 years ago

Not only Mr Werner has fully understood how our economy and financial markets work, but he has also the courage to speak up and clear. Not like some other few economists teaching at Harvard, MIT or Stanford, sometimes granted the economic Nobel price, who understand as well but keep it quiet or even lying to their students, because they want to keep their privilege and high salaries and are happy to be the puppets of our banking system. Thank you Mr Werner, and shame on the others.

539

@freemanbeing1904

5 years ago

what a speech!!! Richard!

118

@18WiddaBullit

5 years ago

Please be so kind to provide the link to prof. Werner’s presentation.

84

@YouHaveAGoodPoint

5 years ago

️genius.

55

@stephenboothby7416

5 years ago

Credit creation still doesn’t negate the law of contracts whereby there needs to be both full disclosure and equal consideration. No-one who gets a loan knows that the money didn’t exist and was created. That equals fraud. Equal consideration where both sides stand to lose an equal amount. Money created out of nothing means only the bank benefits out you either repaying or not as they get to repossess your assets or receive payment plus interest. You are only poorer. That equals cheating. Not a good deal except for bankers

222

==========================

See Also

Luke Ford – Andrew Joyce On The Jewish Question — Apr 17, 2017 — Transcript

David Duke Interviews Dr Andrew Joyce — TRANSCRIPT

Red Ice Radio: Dr Andrew Joyce – The History of Jewish Influence — TRANSCRIPT (Part 1)

Red Ice Radio: Dr Andrew Joyce – The History of Jewish Influence — TRANSCRIPT (Part 2)

TOO – Andrew Joyce’s Podcast – Talmud and Taboo — Part 01 – Jun 30, 2020 — Transcript

Andrew Joyce’s Podcast – T & T No. 1 – The Skype Directory — Jul 15, 2020 — Transcript

Andrew Joyce – T&T No 2 – And then one day… – Jul 20, 2020 — Transcript

Andrew Joyce – T&T No 3 – Kicking Over the Bucket – Jul 27, 2020 — Transcript

Andrew Joyce – T&T 4 – The Man Who Put the Jews on Trial – Aug 3, 2020

Andrew Joyce – T&T 5 – The Return of the Bucket – Aug 5, 2020 — Transcript

Andrew Joyce – T&T 6 – The Antisemite’s Handbook – Aug 11, 2020 — Transcript

Andrew Joyce – T&T 7 – The TOO Takedown – Aug 14, 2020 — Transcript

Andrew Joyce – T&T 8 – SEMITISM – Aug 28, 2020 — Transcript

Andrew Joyce – Trumpism, Bidenism, and the System – Nov 9, 2020 — Transcript

Guide to Kulchur – The Protocols of the Elders of Zion – Andrew Joyce – Nov 22, 2020 — Transcript

Andrew Joyce – BLM – Irish Edition – Dec 31, 2020 – Transcript

Horus – Discussing the ‘Russian Pogroms’ with Andrew Joyce – Jan 20, 2021 — Transcript

911 – The Jews Had Me Fooled: A Jewish Engineered Pearl Harbor

Organized jewry Did 9/11 — The 16th Anniversary, 2017

Know More News — Christopher Bollyn, The Man Who Solved 9/11 — TRANSCRIPT

The Realist Report with Christopher Bollyn – Sep 2018 — TRANSCRIPT

Guns and Butter interviews Christopher Bollyn — The War on Terror – Dec 18, 2019 — Transcript

AE911Truth – Exposing Those Who Covered up the Crime of the Century – May 28, 2023 – Transcript

============================================

PDF Download

Total words in transcript = 2,614

- Total words in post = 3,198

- Total images = xx

- Total A4 pages = xxx

Use your browser to download/export a PDF of this post.

Version History

Version 5:

Version 4:

Version 3:

Version 2:

Version 1: Sat, May 4, 2024 — Published post. Includes Youtube comments (5).